Crypto correlates with equities because both asset classes respond simultaneously to the same macroeconomic signals, not because one drives the other. Federal Reserve interest rate decisions, global liquidity conditions, and institutional capital flows move Bitcoin, the Nasdaq 100, and the S&P 500 in the same direction at the same time. This relationship has grown considerably stronger since 2020, accelerated by the integration of crypto into mainstream portfolios through products like BlackRock's iShares Bitcoin ETF. Understanding why crypto correlates with equities is no longer optional for serious investors. It is a structural feature of modern markets that directly affects diversification, risk management, and portfolio construction.

Why does crypto correlate with equities? the core drivers

The crypto and stock market relationship is grounded in shared macro sensitivity rather than direct causality. When the Federal Reserve tightens monetary policy, risk appetite contracts across all speculative assets simultaneously. Bitcoin falls alongside growth stocks not because equity traders are selling crypto, but because Fed policy decisions affect both asset classes through the same transmission mechanism: the cost and availability of capital.

Three structural forces reinforce this linkage. First, institutional investors now hold meaningful positions in both crypto and equities, and they manage risk across their entire book. When margin calls or redemptions hit, they sell liquid assets across all classes at once. Second, algorithmic trading systems treat Bitcoin as a high-beta risk-on asset, routing similar macro signals through crypto and equity markets simultaneously. Third, shared liquidity infrastructure, including prime brokerage relationships and collateral pools used by both markets, creates mechanical connections that force simultaneous position unwinds during periods of liquidity stress.

The correlation is also asymmetric in a way that matters for risk management. Bitcoin tends to track equity sell-offs closely but often ignores rallies, behaving more like a risk-off indicator than a symmetric hedge. That asymmetry has significant implications for how you size and manage a crypto allocation.

How have historical trends shaped the crypto equity market correlation?

Before 2020, the crypto equity market correlation was effectively negligible. Bitcoin traded on its own narrative, driven by adoption cycles, halving events, and retail speculation largely disconnected from equity market dynamics. That era is over.

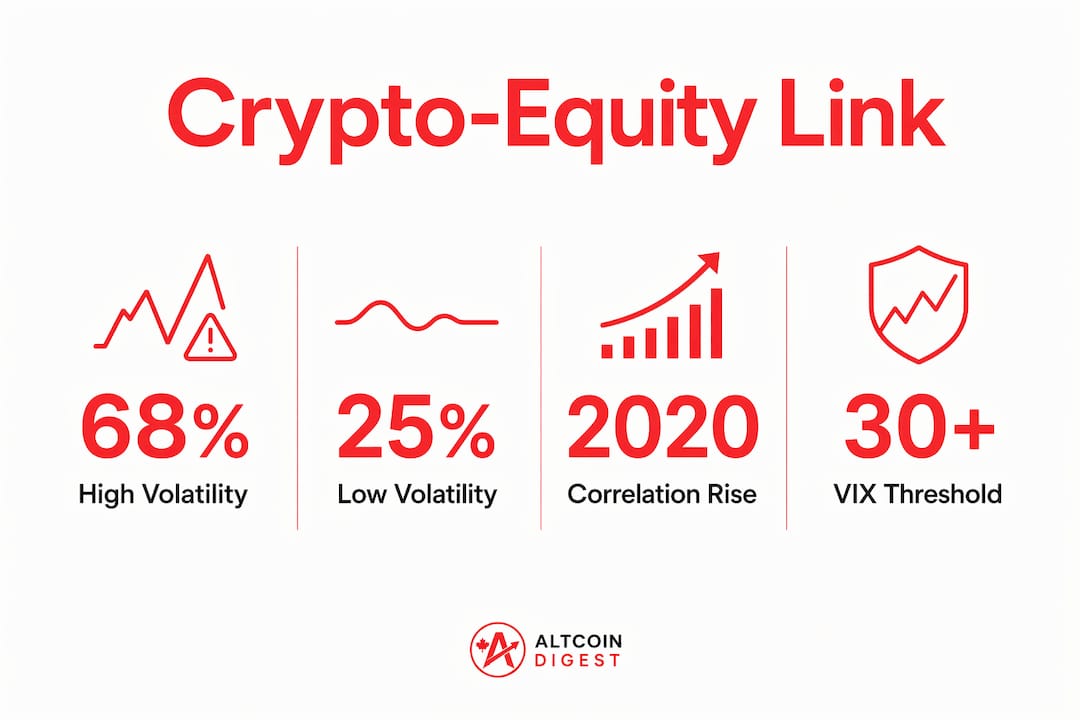

The correlation between Bitcoin and the Nasdaq 100 has risen sharply in recent years. Bitcoin's correlation with the Nasdaq 100 averaged 0.52 in 2025, compared to 0.23 in 2024. On a scale where 1.0 represents identical movement and 0 represents no relationship, a reading of 0.52 is a meaningful positive link. It means roughly half of Bitcoin's price variance in 2025 moved in the same direction as the Nasdaq 100.

The relationship is also regime-dependent, which is the critical nuance most investors miss. Crypto-equity correlation sits around 0.25 during low-volatility periods but spikes to 0.68 during market stress when the VIX exceeds 35. That spike is precisely when diversification is most needed, and precisely when it disappears.

| Market Regime | Approximate Correlation (Bitcoin / S&P 500) | Diversification Benefit |

|---|---|---|

| Low volatility (VIX below 20) | ~0.25 | Moderate |

| Elevated volatility (VIX 20–35) | ~0.45 | Limited |

| Market stress (VIX above 35) | ~0.68 | Minimal |

Pro Tip: Track the VIX alongside your crypto positions. When the VIX moves above 30, historical data suggests the crypto-equity correlation rises sharply, which means your portfolio's apparent diversification may be far smaller than your model assumes.

What structural factors drive the crypto and stock market relationship?

The structural integration of crypto into traditional financial markets has mechanically tightened the correlation. Several specific forces are responsible.

- ETF-driven liquidity integration. Spot Bitcoin ETFs have created a direct channel between crypto and equity market liquidity. Net flows into crypto spot ETFs have reached $87 billion since january 2024. When equity investors rotate into or out of risk assets, those flows now move through the same brokerage infrastructure that handles equity ETFs.

- Algorithmic and quantitative trading. Quant strategies that arbitrage macro signals across asset classes treat Bitcoin as a high-beta equity proxy. When these models detect a risk-off signal, they reduce exposure across both crypto and equities in the same execution cycle.

- Shared prime brokerage and collateral pools. Professional traders use the same prime brokerage relationships for crypto and equity positions. During liquidity tightening, forced simultaneous liquidations across both books amplify the correlation mechanically.

- The volatility paradox. As institutional adoption increases, crypto's idiosyncratic volatility decreases. However, its synchronisation with equity volatility regimes rises. The asset becomes less wild on its own terms but more tightly coupled to the broader market cycle. That is a direct reduction in its hedging utility.

Pro Tip: Monitor dollar funding liquidity conditions, not just equity indices. When dollar funding tightens globally, crypto and equities tend to sell off together regardless of their individual fundamentals. The DXY and SOFR spreads are useful early signals.

The volatility paradox deserves particular attention. Institutional adoption was supposed to mature the crypto market and reduce its correlation with speculative assets. Instead, it has done the opposite. By embedding crypto into the same risk management frameworks, collateral systems, and portfolio models as equities, institutional participation has made the two markets more structurally connected than ever before.

How does investor behaviour affect the crypto-equity correlation?

Investor behaviour is the third pillar of the crypto and stock market relationship, alongside macro policy and structural integration. The mechanism here is the shared speculative cohort.

- Retail and institutional investors participate in both markets simultaneously. The same investor who holds Nvidia or Tesla in a brokerage account often holds Bitcoin or Ethereum in the same portfolio. When sentiment shifts, they adjust both positions at once.

- The Attention factor drives co-movement beyond fundamentals. Research from QuantPedia identifies a specific mechanism: a shared speculative investor cohort drives correlated price movements across crypto and equity venues through collective attention and sentiment, independent of any fundamental economic link.

- Speculative tech equity exposure amplifies the connection. The residual connectedness between crypto and equities is highest for firms dependent on speculative participation, such as high-growth technology companies. Investors who hold both crypto and speculative tech equities embed a compounding risk into their portfolios that standard correlation models underestimate.

- Crypto acts as a high-beta proxy for equity downside. This is the asymmetric correlation in practice. Crypto tracks equity sell-offs more closely than it tracks rallies. In a risk-off environment, Bitcoin often falls harder and faster than the Nasdaq 100, amplifying portfolio drawdowns rather than cushioning them.

- Zero-day-to-expiration options volume signals coordinated positioning. Speculative metrics like zero-day-to-expiration options activity serve as early signals of coordinated capital positioning across crypto and equities that standard correlation models miss entirely.

The practical implication is that crypto does not behave like a separate asset class during the market conditions that matter most to risk management. It behaves like a leveraged expression of the same speculative sentiment driving growth equities.

How can investors apply crypto-equity correlation insights to portfolio management?

Understanding the crypto and stock market relationship changes how you should think about portfolio construction. The correlation is not a fixed number you can plug into a model once and forget. It is a variable that shifts with market regimes.

- Do not assume crypto provides diversification during a crisis. The correlation spikes precisely when markets are stressed, which is when diversification is most valuable. Treating crypto as a crisis hedge based on low-volatility correlation data is a structural error.

- Monitor regime signals actively. The VIX, global dollar liquidity conditions, and Federal Reserve policy guidance are the most reliable leading indicators of when the crypto-equity correlation will tighten. Investors who track these signals can anticipate correlation shifts rather than react to them.

- Size crypto allocations with the high-beta asymmetry in mind. Because crypto tracks equity downside more than upside, a standard mean-variance optimisation will underestimate the tail risk of a combined crypto and equity portfolio. Stress-test your allocation against a scenario where both fall simultaneously.

- Consider whether market correlation is breaking during specific periods. There are episodes where crypto decouples from equities, often driven by crypto-specific catalysts such as regulatory developments or halving cycles. These windows may offer genuine diversification, but they are not reliable enough to anchor a long-term strategy.

- Institutional selling can shift the dynamic quickly. Rising institutional selling pressure in Bitcoin can accelerate correlation with equity drawdowns, particularly when ETF outflows coincide with broader risk-off moves.

Pro Tip: When building a mixed portfolio, model your crypto allocation as a high-beta equity position rather than an uncorrelated asset. That framing produces more accurate risk estimates and more realistic drawdown scenarios.

Key takeaways

Crypto correlates with equities because shared macroeconomic sensitivity, institutional integration, and speculative investor behaviour create structural linkages that tighten most severely during market stress.

| Point | Details |

|---|---|

| Correlation is regime-dependent | The Bitcoin and S&P 500 correlation rises from ~0.25 in calm markets to ~0.68 during high-stress periods. |

| ETF flows mechanically link liquidity | $87 billion in spot crypto ETF flows since 2024 have integrated crypto and equity liquidity pools directly. |

| Asymmetric downside tracking | Crypto follows equity sell-offs more closely than rallies, amplifying portfolio drawdowns in risk-off conditions. |

| Macro policy is the common driver | Federal Reserve decisions move both asset classes simultaneously, not one causing the other. |

| Diversification benefits are limited in crises | Correlation spikes precisely when investors need diversification most, reducing crypto's hedging utility. |

The correlation is more nuanced than most models suggest

The data on crypto-equity correlation is clear enough. What concerns me more is how often investors misread what the data actually means.

The most common error is treating correlation as causation. Equity markets do not move crypto, and crypto does not move equities. Both respond to the same upstream forces: Federal Reserve policy, global liquidity, and speculative sentiment. That distinction matters because it changes how you hedge. If you think equities are pulling crypto down, you might try to hedge by reducing equity exposure. If you understand that both are responding to the same macro signal, you realise that reducing equity exposure alone does not protect your crypto position.

The second error is assuming the correlation is stable. A reading of 0.52 for 2025 is an average across very different market conditions. In a calm, low-volatility quarter, the correlation may be 0.25. In a sharp sell-off, it may be 0.70. Portfolio models that use the annual average are systematically underestimating tail risk.

The third error is expecting institutional adoption to reduce the correlation over time. The volatility paradox suggests the opposite is true. As more capital enters crypto through ETF structures and prime brokerage, the asset becomes more tightly coupled to equity market dynamics, not less. That is not a reason to avoid crypto. It is a reason to model it accurately.

— Lukas

Stay ahead of crypto and equity market dynamics with Altcoindigest

The relationship between crypto and equity markets shifts with every Federal Reserve decision, every ETF flow report, and every change in global liquidity conditions. Staying current on these dynamics requires more than a quarterly portfolio review.

Altcoindigest publishes regular crypto market analysis covering the macro signals, institutional flows, and regulatory developments that drive the crypto-equity correlation. Whether you are managing a mixed portfolio or tracking Bitcoin's relationship with the Nasdaq 100, Altcoindigest provides the focused, timely reporting that investors and analysts need to make informed decisions. Visit Altcoindigest to access up-to-date coverage of the market dynamics shaping crypto and equity performance in 2026.

FAQ

What is crypto market correlation with equities?

Crypto market correlation with equities measures how closely cryptocurrency prices move in relation to equity indices like the S&P 500 or Nasdaq 100. A correlation of 1.0 means identical movement, while 0 means no relationship.

Why does crypto follow stocks during market sell-offs?

Crypto follows stocks during sell-offs because both asset classes respond to the same risk-off triggers, including Federal Reserve tightening and liquidity contraction. Shared institutional investors also sell across both markets simultaneously during stress events.

Does the crypto-equity correlation change over time?

The correlation is regime-dependent, averaging around 0.25 in low-volatility periods but rising to approximately 0.68 when the VIX exceeds 35. Investors should treat it as a variable, not a fixed portfolio input.

Does bitcoin provide diversification against equity market risk?

Bitcoin provides limited diversification during market stress, which is when it is most needed. Its correlation with equities spikes during crises, meaning it tends to fall alongside equities rather than offset losses.

What is the attention factor in crypto-equity co-movement?

The Attention factor is a theory identifying a shared speculative investor cohort that drives simultaneous price movements across crypto and equity markets beyond any fundamental economic link. It explains why crypto and high-growth tech equities often move together even when macro conditions do not fully account for the co-movement.